The Affordable Care Act costs are poised for a dramatic shift, as enrollees in the ACA marketplace brace for considerable financial burdens ahead. With monthly out-of-pocket expenses projected to surge by up to 75% by 2026, the expiration of federal subsidies will leave many scrambling for alternatives. According to policy analysts at KFF, the median insurer rate increase of 18% is slated to hit consumers hard, especially since approximately 93% of marketplace participants benefited from premium tax credits that drastically reduced their healthcare expenses. The end of these subsidies, which helped 19.3 million individuals save an average of $700 annually, is likely to alter the landscape of health care affordability for the many who have relied on these financial aids. As health insurance cost increases loom on the horizon, the impending changes brought by the Affordable Care Act merit urgent attention from prospective and current enrollees alike.

The impending costs associated with the ACA marketplace will have significant implications for health care access in the near future. Rising insurance premiums combined with the planned expiration of financial support mechanisms, such as premium tax credits, threaten to make healthcare prohibitively expensive for many families. The looming health insurance cost increases could push vulnerable individuals away from necessary coverage just when they might need it most, leading to a distressing cycle of unmet health needs. Moreover, with substantial alterations in the health insurance framework anticipated due to recent Affordable Care Act changes, many may find themselves seeking alternatives to ensure they maintain access to essential medical services. Thus, the evolving landscape of health insurance costs and Medicaid cuts compels a closer examination of how these factors intertwine to impact healthcare affordability for millions.

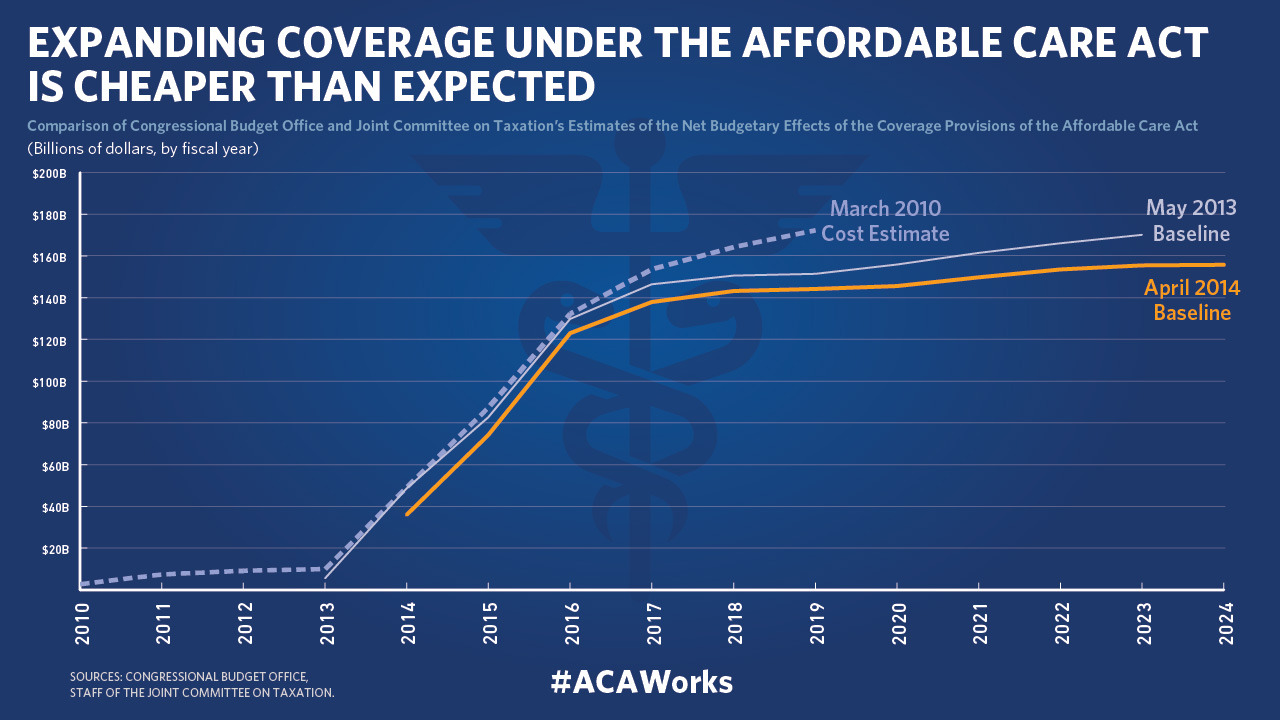

Impact of Affordable Care Act Costs on Everyday Americans

The anticipated increase in costs associated with the Affordable Care Act (ACA) marketplace is poised to significantly affect the financial well-being of many Americans. With rising monthly out-of-pocket expenses and the loss of premium tax credits, approximately 19 million enrollees who benefited from these subsidies are now facing financial uncertainty. Experts predict a staggering rise in monthly costs, potentially reaching 75% by 2026, which could deter many individuals from maintaining their health insurance plans.

Notably, the expiration of federal subsidies at the end of 2025 will exacerbate this situation, forcing many families to compromise on their health coverage. The promise of affordable care provided by the ACA is at risk, as rising costs may lead to a significant decrease in enrollment, especially among those who previously relied on these financial aids to manage their healthcare expenses. Such trends will not only affect individual health outcomes but also the larger healthcare system, as fewer enrollees could lead to increased premiums for those remaining in the marketplace.

Why Insurers Are Increasing Rates: A Closer Look

Insurers are pushing for hefty rate increases as they attempt to navigate the challenging landscape of the healthcare marketplace. With an average request for an 18% increase, the rationale hinges on multiple factors, including rising medical costs, increased demand for specific medications, and the expiration of premium tax credits. Insurance providers highlight that the demand surge for GLP-1 medications, combined with systemic issues like worker shortages, has escalated operational costs, thus necessitating these sharp price hikes.

Moreover, with healthcare providers consolidating, insurers often face higher costs due to the increased market power of fewer providers. This consolidation typically results in less competition and, consequently, higher prices being passed on to consumers. As a result, the financial strain on individuals needing health coverage is likely to increase, contrasting sharply with the original aims of the ACA to render health care more affordable and accessible for all.

Consequences of Premium Tax Credits Expiration

The looming expiration of premium tax credits is set to send shockwaves through the ACA marketplace, with a vast majority of enrollees likely feeling the burden. The Center on Budget and Policy Priorities reports that approximately 93% of marketplace participants have benefited from these credits, reflecting their crucial role in making health insurance affordable. Without these credits, families face the prospect of significant premium increases, with potential monthly costs rising by $100 to $200, a burden that many may find untenable in the current economic climate.

As individuals begin to weigh their options for health insurance enrollment, the prospect of paying full premiums without the safety net of tax credits will influence their decisions significantly. For many, the economic implications could result in either foregoing necessary healthcare services or entirely dropping out of the marketplace, which would have further implications for those who remain—larger pools of high-need patients, ultimately driving prices even higher.

The Interplay Between ACA Changes and Medicaid Cuts

The changes to the Affordable Care Act are intertwining with impending cuts to Medicaid, creating a perfect storm that threatens access to affordable healthcare for vulnerable populations. As policymakers consider reductions in social safety nets, those who rely on Medicaid and ACA coverage may find themselves without crucial avenues for medical assistance. These cuts could disproportionately impact low-income families, the disabled, and other marginalized communities, further entrenching health inequities.

As Jennifer Sullivan from the Center on Budget and Policy Priorities indicates, the challenge of obtaining affordable healthcare is growing. Recent legislative requirements mandating more stringent eligibility checks for ACA plans will likely contribute to reduced enrollment figures, while disenrollment from Medicaid will leave many without any insurance coverage at all. This reality could lead to increased emergency room visits, raising healthcare costs across the board, which ultimately places a heavier financial burden on the healthcare system overall.

Future of Health Care Affordability and Accessibility

The future of health care affordability remains precarious as pressures mount from both policy changes and economic realities. As mentioned, rising costs associated with premiums and the potential loss of subsidized insurance threaten to diminish the gains made since the Affordable Care Act’s inception. The importance of maintaining accessible healthcare options for all cannot be overstated, particularly in light of ongoing concerns about rising infant mortality rates and life expectancy across the country.

Healthcare advocates continue to lobby for the preservation of essential tax credits and the protection of Medicaid as pillars of health care accessibility and affordability. Engaging communities on the potential consequences of losing these supports is crucial for mobilizing a collective response to protect essential coverage options. Without significant intervention to maintain or expand these programs, health disparities in the U.S. may widen, underscoring the need for renewed commitment to health care reform.

The Role of Community Engagement in Health Insurance Awareness

Awareness and understanding of health insurance options are critical, especially as changes loom over the ACA marketplace. Organizations like the Center on Budget and Policy Priorities are engaging communities across the nation to educate them about the impacts of potential policy changes, including the expiration of premium tax credits. This education is vital for ensuring that individuals are prepared to respond to upcoming challenges, including financial adjustments when shopping for insurance during open enrollment.

Community outreach efforts can also aid in identifying those at risk of losing coverage and help them navigate complex healthcare systems. By effectively disseminating information and addressing misconceptions about the ACA, health coverage advocates can empower consumers to make informed decisions, ultimately working to maintain participation in the marketplace when costs rise.

Understanding the Dynamics of ACA Marketplace Enrollment

Enrollment numbers in the ACA marketplace have been variable and often driven by economic factors, educational outreach, and policy changes. The rapid increase to over 20 million enrolled individuals in recent years showcases the effectiveness of expanded premium tax credits introduced in 2021. However, with these credits set to expire and recent policy changes complicating the enrollment process, there is potential for a downturn in participation.

Monitoring these dynamics is essential for understanding how financial pressures are influencing individual decisions. As individuals evaluate their healthcare needs and affordability, understanding the factors that drive enrollment, such as income fluctuations and the stability of financial assistance, will be crucial in predicting future trends in marketplace participation.

Health Care Affordability: Looking Beyond Premiums

While premium costs are a significant factor in overall health care affordability, they are just one piece of a much larger puzzle. Out-of-pocket expenses, deductibles, and copayments all contribute to the financial landscape of accessing healthcare. As costs increase due to the expiration of premium tax credits and rising insurer rates, individuals may find their financial burdens growing beyond just the premiums they pay monthly.

Recognizing that healthcare affordability encompasses a range of costs is crucial for understanding the implications of the changing ACA landscape. Ensuring that affordable care doesn’t just mean access to insurance, but also manageable out-of-pocket costs, is key to maintaining overall health equity. Addressing these broader financial issues will require comprehensive policy strategies that enhance affordability at every level of healthcare.

Navigating Health Care Decisions in an Uncertain Landscape

The decision to purchase health insurance is becoming increasingly complicated for many Americans, particularly with impending changes to the Affordable Care Act. As families face the potential expiration of premium tax credits and dramatic increases in premiums, the once straightforward choice to obtain coverage is now riddled with uncertainty. Individuals must weigh their healthcare needs, financial ability, and the risks of being uninsured against the backdrop of a rapidly changing health care system.

For many, stories of fear and anxiety underscore the challenges faced when navigating these difficult decisions. Ensuring individuals have access to the right information is critical in empowering them to make conscious health decisions in the face of such uncertainty. As the landscape shifts, supporting consumers through education and resources will be vital to restoring confidence in making health care choices.

Frequently Asked Questions

What factors are contributing to increased Affordable Care Act costs in 2026?

The increase in Affordable Care Act costs in 2026 is primarily driven by the expiration of premium tax credits, which have significantly subsidized expenses for many enrollees. Insurers are also proposing a median rate increase of 18%, attributed to rising health care costs, tariffs affecting pharmaceuticals, and increased demand for specific medications, among other factors.

How will the expiration of premium tax credits impact ACA marketplace rates?

The expiration of premium tax credits at the end of 2025 is expected to substantially increase ACA marketplace rates for nearly 20 million enrollees. With these credits disappearing, many individuals who previously paid little or no premiums will face higher insurance costs, potentially driving them out of the marketplace.

What has been the impact of health insurance cost increases on ACA enrollees?

Health insurance cost increases, projected to reach as much as 75% by 2026 for many ACA enrollees, could limit access to affordable health care. The loss of premium tax credits will exacerbate these financial burdens, making it harder for individuals to maintain their health insurance coverage.

Are Medicaid cuts affecting the affordability of health care under the Affordable Care Act?

Yes, proposed cuts to Medicaid could further strain health care affordability under the Affordable Care Act. As Medicaid provides a safety net for many low-income individuals, these cuts could lead to higher rates of uninsured and underinsured individuals, ultimately increasing overall health care costs for everyone.

What are the long-term implications of the Affordable Care Act changes on health insurance accessibility?

The changes to the Affordable Care Act, including the expiration of premium tax credits and potential Medicaid cuts, may lead to decreased enrollment in marketplace plans. This could result in a higher concentration of individuals with significant health care needs left in the pool, raising premiums further and reducing overall accessibility to affordable health insurance.

How have health care affordability issues influenced enrollment in ACA marketplace plans?

Health care affordability has a direct impact on enrollment in ACA marketplace plans. The introduction of premium tax credits significantly boosted enrollment by making insurance more accessible. However, as these credits are set to expire, many individuals are likely to reconsider their options, leading to potential declines in enrollment.

What role do health insurance cost increases play in the broader health care system?

Health insurance cost increases under the Affordable Care Act impact not only individual enrollees but also the broader health care system. When individuals forgo insurance due to rising costs, they often delay necessary care and rely on emergency services, which drives up costs for everyone and can negatively affect public health outcomes.

| Key Point | Details |

|---|---|

| Significant Cost Increases | In 2026, out-of-pocket expenses for ACA marketplace users may rise by 75% due to ending federal subsidies. |

| Insurance Rate Increases | KFF reported a median proposed rate increase of 18% from insurers, more than twice the previous year’s increase. |

| Impact of Premium Tax Credits | 93% of marketplace enrollees benefited from $700 average annual savings due to these credits, which are set to expire at the end of 2025. |

| Reasons for Rate Increases | Insurers cite rising healthcare costs, tariffs, expiration of tax credits, and demand for certain drugs as factors for rate hikes. |

| Potential Drop in Enrollment | Higher costs may push many individuals out of the marketplace, reducing the pool of relatively healthy enrollees. |

| Broader Implications of Uninsured | Uninsured individuals may resort to emergency care, leading to higher costs for everyone. |

| Concerns of Individuals | Individuals like Amy Bielawski express fear about increased costs affecting their ability to access necessary healthcare. |

| Legislative Challenges | Recent policy changes may restrict enrollment and eligibility, further reducing the number of people in ACA plans. |

Summary

Affordable Care Act costs are poised to rise dramatically in the coming years, particularly with the elimination of federal subsidies in 2026. This situation will leave millions vulnerable to increased insurance premiums and potential loss of coverage. With a predicted median insurer rate hike of 18% for the next year, along with expiring premium tax credits that have financially supported many enrollees, this perfect storm of factors raises alarms about healthcare affordability. As costs continue to escalate, it is critical for stakeholders to address these issues to ensure that affordable health insurance remains accessible to all Americans.